The Stellar Improvement Basis, builders of the Stellar community, launched a monetary inclusion framework for judging the efficacy of rising market blockchain tasks. The framework was developed in cooperation with consultants PricewaterhouseCoopers Worldwide (PwC) and was defined in a white paper revealed on September 25.

Utilizing this framework, the groups concluded that blockchain funds options considerably elevated entry to monetary merchandise by reducing charges to 1% or much less. Additionally they discovered that blockchain merchandise have elevated the pace of funds and helped customers to keep away from inflation.

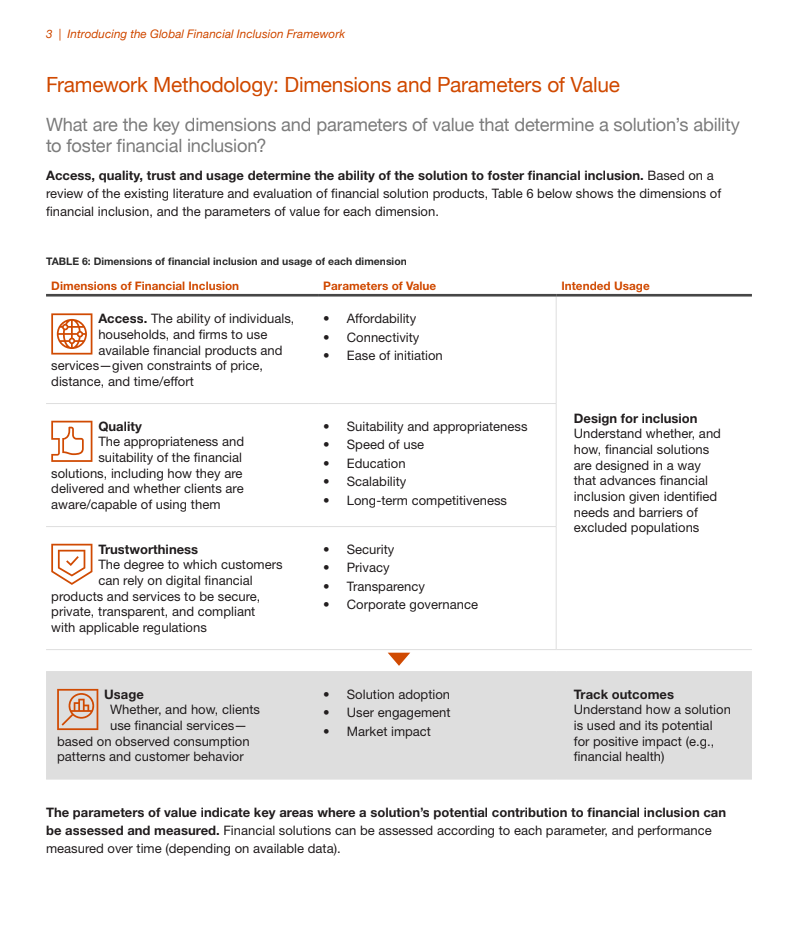

Monetary inclusion framework parameters. Supply: Stellar, PwC.

Some blockchain builders declare their merchandise can improve “monetary inclusion.” In different phrases, they are saying their merchandise can present providers to unbanked folks dwelling within the growing world. Making this declare has grow to be an efficient approach for some Web3 tasks to realize funding. For instance, the United Nations Worldwide Youngsters’s Emergency Fund (UNICEF) has listed eight blockchain tasks that it has helped fund to date based mostly on this concept.

Nevertheless, of their paper, Stellar and PwC argued that tasks can fail to reinforce monetary inclusion in the event that they don’t have a framework for evaluating what is required for fulfillment. “As with all technological innovation, the necessity for strong governance and accountable design rules are key to profitable implementation,” they stated.

To assist foster this governance, the 2 groups proposed a framework to evaluate whether or not a venture will probably promote monetary inclusion. The framework consists of 4 parameters: entry, high quality, belief and utilization. Every of those parameters is damaged down into additional sub-parameters. For instance, “entry” is damaged down additional into affordability, connectivity, and ease of initiation.

Every rationalization of a sub-parameter features a proposed approach of measuring it. For instance, Stellar and PwC listing “# of CICO [cash in/cash out] areas inside related goal inhabitants area” as a approach of measuring the “connectivity” metric. That is supposed to assist be certain that tasks can scientifically measure their effectiveness as a substitute of counting on guesswork.

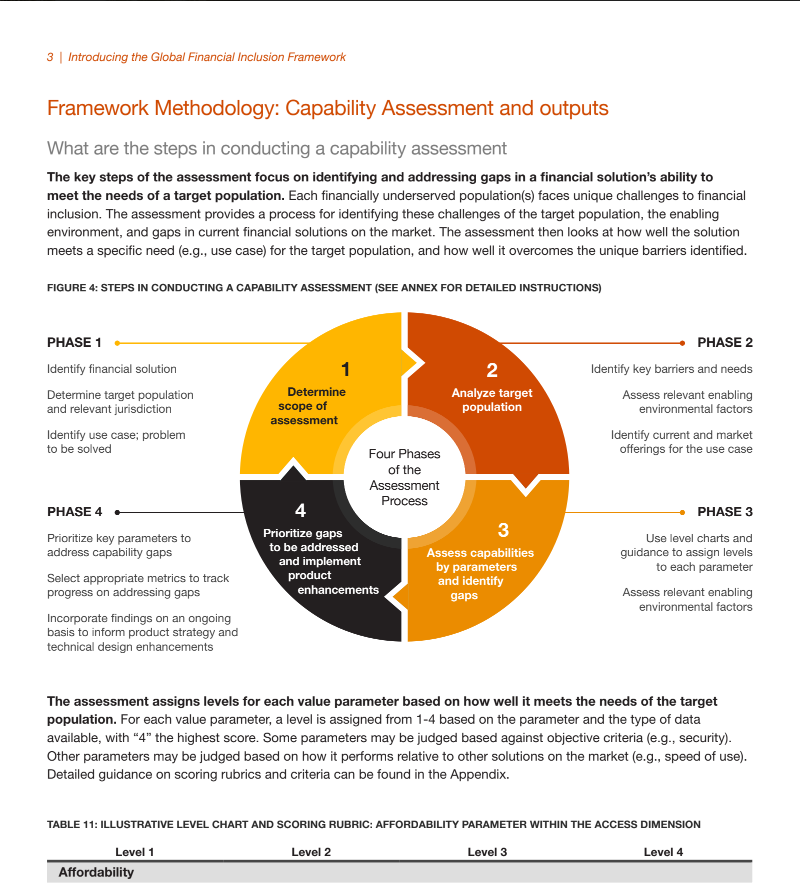

The groups additionally prompt a four-phase evaluation course of that tasks ought to endure to resolve a monetary inclusion downside. The venture ought to establish an answer, goal inhabitants, and related jurisdiction within the first part. In part 2, they need to establish limitations stopping the goal inhabitants from receiving monetary providers. In part 3, they need to use “degree charts and steerage” to find out the largest roadblocks to onboarding customers. And within the closing part, they need to implement options that “prioritize key parameters” to make the best use of funds.

Phases to implement monetary inclusiveness framework. Supply: Stellar, PwC.

Utilizing this framework, the groups recognized at the least two blockchain options which have confirmed to be efficient at enhancing monetary inclusion. The primary is funds. The groups discovered that conventional monetary apps cost a mean of two.7-3.5% to ship cash between the US and the market being studied, whereas blockchain-based options charged 1% or much less, based mostly on a examine of 12 functions working in Colombia, Argentina, Kenya, and the Philippines. They discovered that these functions elevated entry by making digital funds accessible to individuals who in any other case couldn’t afford them.

The second efficient answer they discovered was financial savings. The workforce claimed {that a} stablecoin utility in Argentina permits customers to spend money on an inflation-resistant digital asset, serving to them to protect their wealth after they in any other case would have misplaced it.

Stellar community has been on the forefront of fee inclusion in underserved monetary markets. In December, it introduced a program to assist charity organizations distribute funds to assist Ukrainian refugees fleeing struggle. On September 26, they introduced a partnership with Moneygram to supply a non-custodial crypto pockets that can be utilized in over 180 nations. Nevertheless, some monetary and financial specialists have criticized the usage of cryptocurrency in rising markets. For instance, a paper revealed by the Financial institution of Worldwide Settlements on August 22 argued that cryptocurrency has “amplified monetary dangers” in rising market economies.