The Federal Commerce Fee (FTC) is laying out the scope and strategies utilized by crypto fraudsters to rack up a billion {dollars} in illicit features.

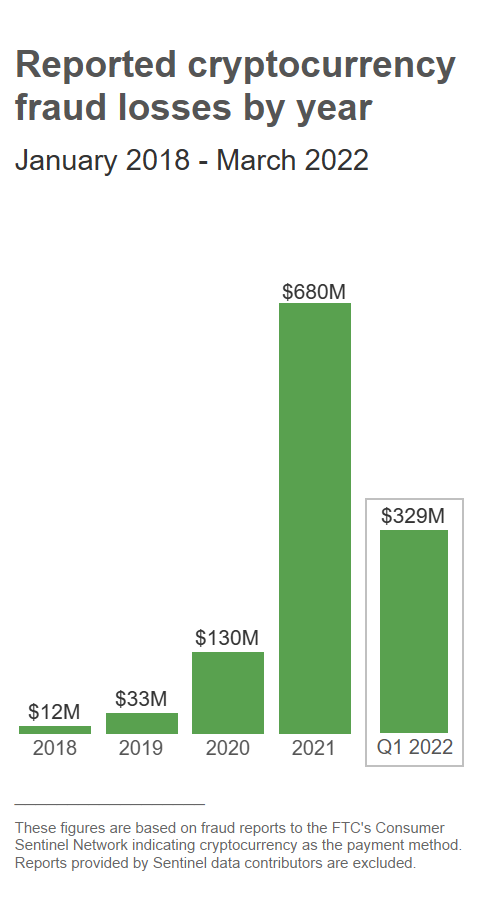

In line with a brand new client safety report, the FTC says that for the reason that starting of final yr, over 46,000 individuals had greater than $1 billion stolen through cryptocurrency scams, with victims dropping a median quantity of $2,600.

The report supplies a breakdown of which digital property have been used to pay the thieves, with Bitcoin (BTC) taking the overwhelming majority at 70%, adopted by stablecoin Tether (USDT) at 10% and main altcoin Ethereum (ETH) at 9%.

The FTC goes on to say that scammers choose to make use of digital property for his or her schemes attributable to lack of banking oversight, incapacity to reverse a transaction, in addition to the typical client’s lack of understanding about crypto and blockchain know-how.

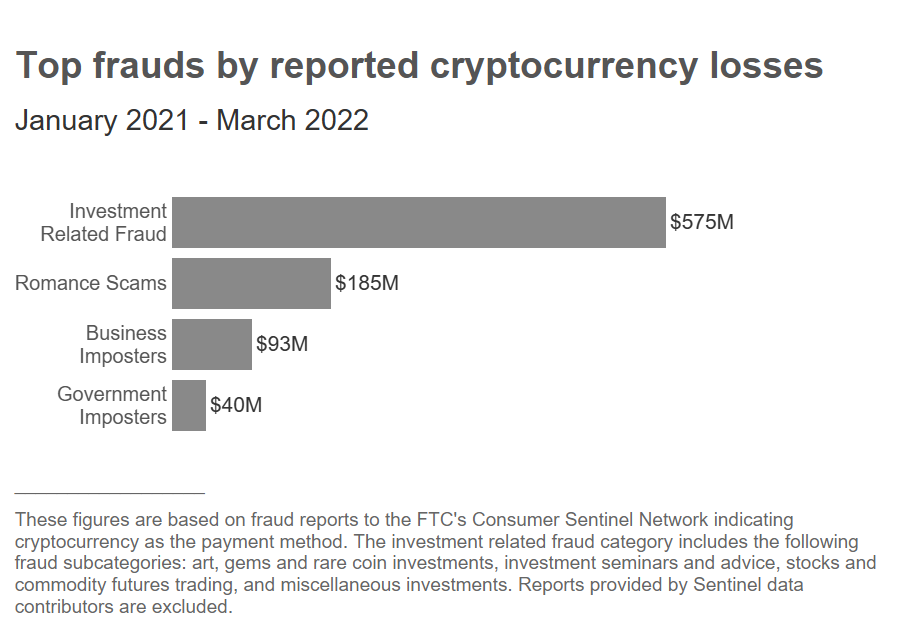

Relating to the varieties of scams and losses, the report says,

“Since 2021, $575 million of all crypto fraud losses reported to the FTC have been about bogus funding alternatives, way over some other fraud sort…

Enterprise and authorities impersonation scams are subsequent with $133 million in reported crypto losses since 2021. These scams can begin with a textual content a few supposedly unauthorized Amazon buy, or an alarming on-line pop-up made to appear like a safety alert from Microsoft.”

The report additionally provides examples of how refined a number of the ruses are, with customers seemingly capable of observe the expansion of their investments and even make a nominal check withdrawal with a view to achieve belief.

Examine Value Motion

Do not Miss a Beat – Subscribe to get crypto e mail alerts delivered on to your inbox

Observe us on Twitter, Fb and Telegram

Surf The Each day Hodl Combine

Featured Picture: Shutterstock/SerGRAY/Natalia Siiatovskaia