newbie

Rates of interest play a pivotal position in our monetary lives, impacting all the pieces from our financial savings to the price of borrowing cash. This text goals to delve into two basic kinds of rates of interest: easy and compound. To make knowledgeable monetary selections, it’s crucial to know the excellence between them, how they’re calculated, and their potential affect in your funds.

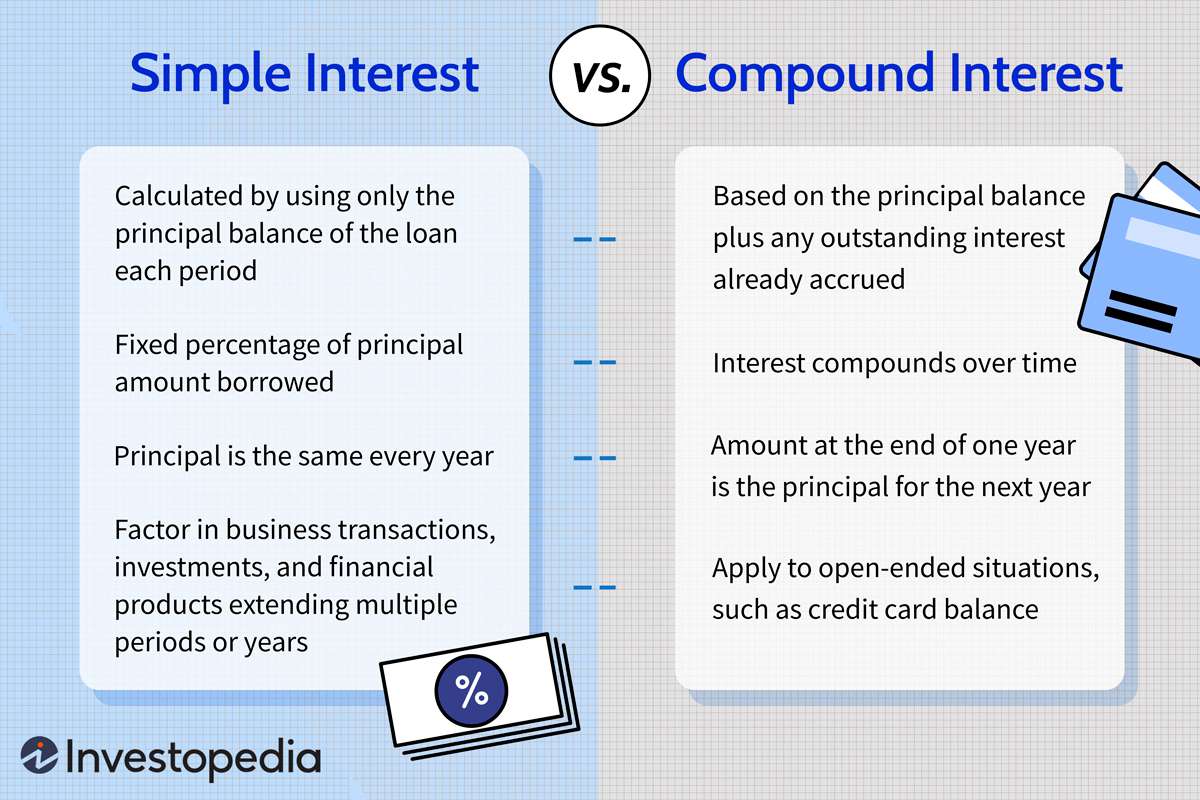

Easy curiosity is an easy idea computed on the unique amount of cash (principal) with out bearing in mind any beforehand accrued curiosity. However, compound curiosity takes under consideration not solely the principal quantity but in addition the curiosity that has accrued over time, resulting in quicker development. This text will introduce you to their respective formulation, providing a transparent understanding of the best way to calculate compound and easy curiosity. Moreover, I’ll define the important thing distinction between easy and compound curiosity.

My title is Daria Morgen, and I’ve been within the crypto trade since 2014. Having the ability to calculate compound curiosity has been an incredible assist in my very own funding journey, and I hope this text can assist you to boost your personal buying and selling methods, too.

What Is Easy Curiosity?

Easy curiosity is calculated on the preliminary amount of cash deposited or borrowed. It doesn’t think about any curiosity beforehand earned or charged. Many monetary establishments, like banks and credit score unions, use this mannequin for sure merchandise, resembling scholar loans and a few kinds of financial savings accounts.

How Does Easy Curiosity Work?

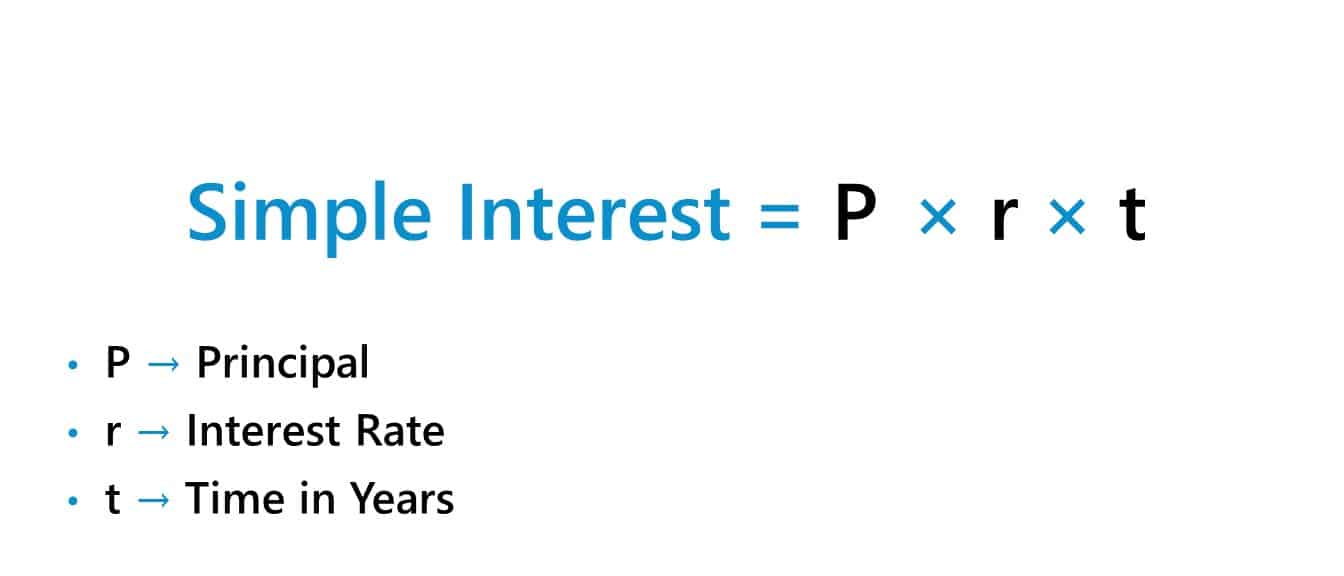

The straightforward curiosity method is fairly easy:

Easy Curiosity = Principal * Annual Curiosity Fee * Time

This method tells us that the curiosity is a product of the principal quantity, the annual rate of interest, and the time interval for which the cash is borrowed or invested. The time is usually expressed in years.

As an example, you probably have a bank card that fees easy curiosity, you’re solely ever charged curiosity on the principal stability, no matter any accrued curiosity from earlier billing intervals.

Easy Curiosity Instance

Let’s assume you deposit $1,000 in a financial savings account with an annual rate of interest of 5% and depart the cash there for one yr. The straightforward curiosity earned could be:

Curiosity = $1,000 * 5% * 1 = $50

On the finish of that yr, you’d have $1,050 in your financial savings account.

What Is Compound Curiosity?

Compound curiosity, however, might be regarded as “curiosity on curiosity.” It takes under consideration each the principal stability and the curiosity that has beforehand been added.

Compound curiosity is frequent in lots of monetary merchandise like bank cards, financial savings accounts, certificates of deposit (CDs), and even some scholar loans.

How Does Compound Curiosity Work?

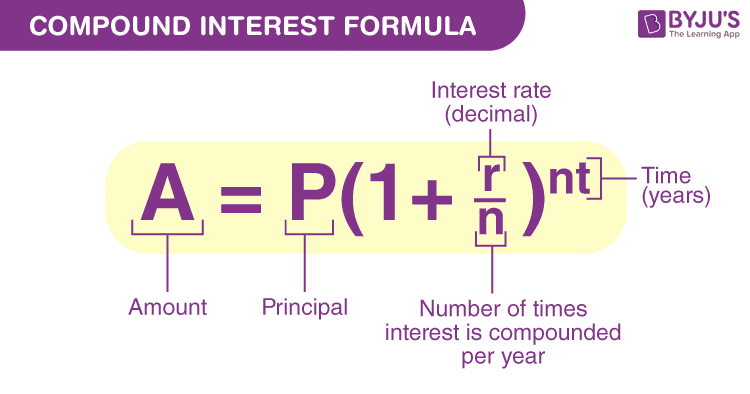

The method for compound curiosity is a little more advanced than the easy curiosity method:

Compound Curiosity = Principal * (1 + Annual Curiosity Fee / Variety of Compounding Intervals)^(Variety of Compounding Intervals * Time) – Principal

This method demonstrates that the curiosity is calculated on the preliminary quantity and the accrued curiosity from earlier time intervals. The variety of compounding intervals can range. It might be yearly, semi-annually, quarterly, and even every day.

Compound Curiosity Instance

Let’s take the identical $1,000 deposit at an annual rate of interest of 5%, however this time, the curiosity is compounded yearly. On the finish of 1 yr, your financial savings account would have:

Curiosity = $1,000 * (1 + 5%/1)^(1*1) – $1,000 = $50

This seems the identical as the easy curiosity instance, proper? That’s as a result of the results of compound curiosity actually begin to present over longer intervals of time. Let’s say you permit the cash for 5 years as a substitute:

Curiosity = $1,000 * (1 + 5%/1)^(1*5) – $1,000 = $276.28

On the finish of 5 years, you’d have $1,276.28 in your financial savings account. That’s considerably greater than you’d have with easy curiosity.

Easy Curiosity vs. Compound Curiosity. Which One to Select?

Whether or not easy or compound curiosity is healthier for you is dependent upon whether or not you’re borrowing or investing cash.

If you wish to borrow cash, you’d usually desire a mortgage with a easy curiosity method, as you’d find yourself paying much less over the mortgage time period in comparison with compound curiosity. It is because you’re solely being charged curiosity on the unique principal, not on any accrued curiosity.

Conversely, when you’re investing or saving, compound curiosity might be extra useful because it permits your cash to develop at a quicker fee over time as a result of impact of compounding. Which means that you earn curiosity not solely in your authentic funding but in addition on the curiosity that your funding has already earned.

Easy or Compound Curiosity for Crypto

Relating to investing in cryptocurrencies, the selection between easy and compound curiosity is dependent upon your monetary objectives and danger tolerance. If a crypto platform presents curiosity on holdings, compound curiosity may result in extra substantial development over time. Nevertheless, as with every funding, it’s essential to know the dangers and potential fee of return.

In conclusion, understanding the variations between easy and compound curiosity is crucial for making knowledgeable monetary selections. It might probably tremendously affect how a lot you find yourself paying on loans or incomes on investments over a time period.

FAQ

What’s the method for calculating curiosity?

The method for calculating easy curiosity is kind of easy: Easy Curiosity = Principal * Annual Curiosity Fee * Time. It’s calculated on the preliminary principal quantity with out contemplating the curiosity that accumulates over time.

In distinction, the compound curiosity method is extra advanced: Compound Curiosity = Principal * (1 + Annual Curiosity Fee / Variety of Compounding Intervals)^(Variety of Compounding Intervals * Time) – Principal. Compound curiosity is calculated on the preliminary principal and likewise on the accrued curiosity from earlier intervals.

How are easy curiosity and compound curiosity completely different?

The important thing distinction between easy curiosity and compound curiosity lies in how the curiosity accumulates. Easy curiosity is calculated solely on the unique quantity (principal) that you just deposit or borrow, whereas compound curiosity is calculated on the principal quantity and any accrued curiosity. Which means that with compound curiosity, you earn or owe curiosity on the curiosity.

Which kind of curiosity can earn extra money over the long run?

Over the long run, compound curiosity can earn extra money. That is as a result of impact of compounding, the place you earn curiosity on each the cash you’ve initially invested and the curiosity you’ve already earned.

How do easy rates of interest have an effect on month-to-month funds on loans?

For private loans or some other mortgage that makes use of easy curiosity, the month-to-month cost largely stays the identical all through the mortgage time period. It is because the curiosity is calculated solely on the unique principal, and the general mortgage quantity doesn’t enhance as a result of further cash generated by accrued curiosity.

Does the frequency of compounding curiosity have an effect on how a lot curiosity you earn or owe?

Sure, the frequency of compounding can considerably affect the quantity of curiosity earned or owed. The extra incessantly curiosity is compounded, the extra curiosity accumulates, offered that the annual fee stays the identical. For instance, curiosity compounded every day will accrue greater than curiosity compounded yearly.

How does the Annual Share Fee (APR) relate to easy and compound curiosity?

The Annual Share Fee (APR) is a standardized means of expressing the price of borrowing cash, which incorporates each the rate of interest and any charges related to the mortgage. For loans with easy curiosity, the APR and the rate of interest will usually be the identical. Nevertheless, for loans with compound curiosity, the APR shall be greater than the said rate of interest as a result of impact of compounding.